Ultimate Guide to Saving for Taxes in private practice

You’re in the right place if you have a private practice (or if you’re starting a private practice) and if you want to make sure that you actually have enough money set aside to pay your business taxes.

Before I get into it, I wanted to tell you a little bit more about myself and why I am so passionate about emotionally literate financial coaching.

I’m Linzy Bonham and I’m a private practice therapist. I’m also the creator of Money Skills for Therapists, which is an online course that helps therapists change their relationship with money and create a money system for their private practice that meets their needs. My ultimate goal is to help you feel calm and confident about your private practice finances.

I wrote this article about how to save enough for taxes to show you that it’s possible to have a different relationship with your money and to show you that money skills are just like any other skill that you can learn with the right support, dedication, and an easy-to-use system.

>>>Click here for a free taxes calculator that I’ll talk about later in this article<<< (((email opt-in)))

Make sure to write down any questions that come up for you as you go through the article. And if I haven’t answered your questions by the end, hop over to my private Facebook group for therapists and I’ll be happy to answer all of your questions there.

Okay, let’s get to it. Setting aside enough for taxes in five easy steps.

Private Practice Finances are Confusing

I love helping other therapists with money. And I’m really glad that you’ve found my ultimate guide to saving enough for taxes. So let’s start with the problem.

Taxes can be really confusing and starting a private practice can be really daunting because there’s so much to do and learn. Taxes are just one of the many things to do and learn when you’re starting your private practice, or even if you’ve been in private practice for a while! Then there are all these things to learn about marketing and client records and keeping track of finances.

So taxes often end up being one of those pieces that can be quite easy to ignore in the whole mix of all those things that we constantly have to deal with as business owners. It’s understandable to put off saving for taxes when there are other pressing things and tax season is still months away.

When you first start your private practice, it can also be tricky to figure out your business finances because there’s not a lot of cash flow coming in. This can make it really hard to put money aside. You might only be making a couple hundred dollars at first, after you pay your rent. So when you’re starting off like that, it’s easy to just take that money home, instead of putting aside any tax money, because you need it if you’re starting with a small practice.

That cycle tends to continue on and on. Most private practice therapists don’t actually stop and build the habit of managing their taxes in a more proactive way as their practice grows. Without having a clear system, your tax money gets all mixed up in the rest of your private practice income.

I kind of picture it in the same way that I describe what I’m talking to clients about enmeshment. You can’t tell where your business money ends and your personal money begins, and nothing is really earmarked. So it all just kind of gets spent and there’s no clarity at all about what is for what.

The Pain of a Successful Private Practice

The other confusing and daunting piece about taxes is that as you make more money, you need to pay more taxes. So for some of us, there actually can be pain in success as your practice grows.

You might have been paying a certain amount of taxes and suddenly your practice starts to grow. You have a good year. You make way more money than you did last year, and now you owe way more money. You didn’t anticipate that, so you didn’t put the money aside. This can all be very, very painful.

Not Saving Enough For Taxes

Some therapists tell me that they just don’t know how to pay themselves or how much to put away for taxes. So they end up not saving nearly enough. And that can be a really common thing when we’re managing our private practice taxes – to put some money aside, because you know that you owe something, but it’s not nearly enough. You might even know that it’s not nearly enough, but sometimes I see this kind of hopeful avoidance that it’ll just work out in the end somehow.

Another private practice therapist told me last year that they made a lot more money, but when tax time came around, they had a huge tax bill and that really, really hurt. I’ve even heard of therapists who really level up their business and end up being taxed extra taxes so that they owe sixteen thousand dollars or even fifty thousand dollars if they’ve really done something to grow their business. That is an extremely painful additional tax bill to pay.

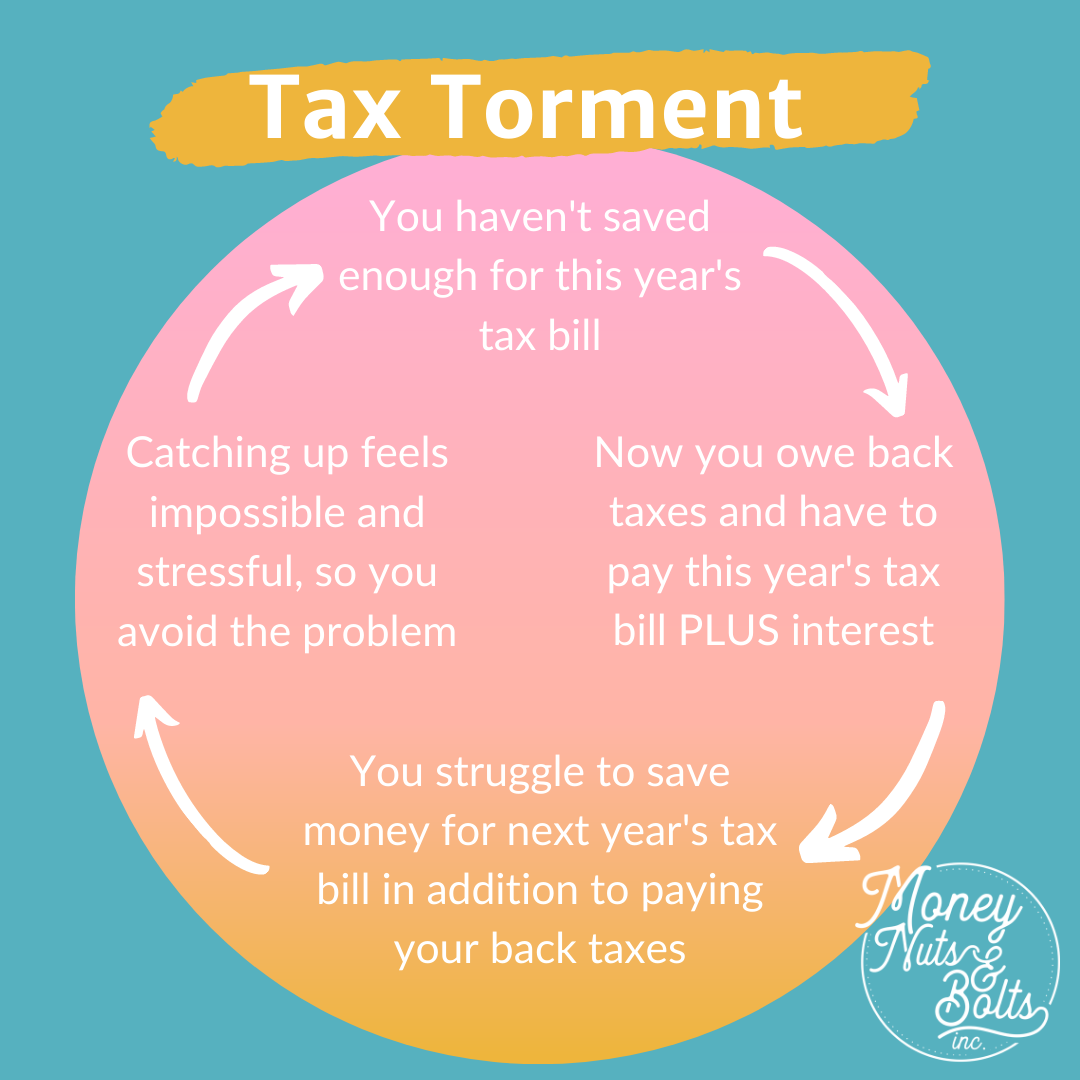

Cycle of Torment

You can get into this cycle of pain if you don’t save enough money for taxes. You can end up needing to pay last year’s taxes, plus the interest that you’re charged, and trying to save for this year’s taxes, all with the money you earned this year. For those of you who have been in this position, I’m sure you could relate to just how painful that actually is, where you get a tax bill that you can’t pay, which turns into some sort of payment plan with the CRA in Canada or the IRS in the US.

So now you’re paying off last year’s expenses with the money you’re making now. But you also have to be saving now for next year’s taxes, or for your quarterly taxes if you start to pay quarterly. You end up in this backlog of owing so much and having to put so much aside that it can really severely impact your income and just really suck. It ends up feeling like you’re paying more than double taxes because of that penalty interest that you have to pay.

It can be extremely hard to catch up, let alone get ahead and save for retirement, sick leave, vacation, or anything else. The emotional weight of this, from people that I’ve worked with who get into this situation, is very scary. To know that you owe so much and you don’t have the money can be very shameful. People can really be afraid of it, so they start avoiding it. You get into a cycle of avoidance where maybe you don’t file because you really don’t have the money, and that goes on and on. That can get you into really bad places with the government.

This is Normal

This is so normal, and this is something that I really want you to take away today, that it is really normal to be confused about taxes and finances. It’s really normal not to know how to just create a system and not knowing how to do these things because no one teaches us.

When I started my private practice, I remember as I started to come across these problems and look for information about how to do this, it really wasn’t out there.

How much?

How do you do that?

How do you know that you’re saving right amounts?

That information is not out there.

I mean, as therapists – I’m trained as a social worker – we are educated on how to sit with someone in their pain, how to help them feel hope. We’ve been taught all these amazing interventions to work with. But nowhere in school or any training have I been taught how to manage my finances. And that is the case for most of us. We’re in the profession because we care about people, not because we wanted to be business people. It’s very rare that somebody has an MBA and is also a therapist. It’s a very rare overlap of interests.

On top of that, most of us were never taught how to manage money, period. We weren’t taught at home. We weren’t taught in our high school. So on top of not knowing how to manage business finances, there’s just a vacuum in our society with skills around money. We just are not taught how to manage money. It’s something that everybody needs but doesn’t get, and yet, you will learn quadratic equations. So there are problems with our culture and our education system – that is not about you.

You Can Do This

That leaves us all kind of scrambling and having to figure these things out on our own. I want you to know that you can do this. This is my little pep talk portion, and by you, I mean you sitting in your office who might be feeling a little bit overwhelmed right now and daunted. There’s a very doable series of steps that I’m going to lay out here. It’s all about implementing those steps, making it happen, and if you follow the steps that I laid out, you will absolutely save enough for taxes. You will absolutely not have to worry about this, and you’ll be able to focus your energy on other things that you care about much more.

Five Easy Steps To Saving For Taxes

So today, I’m going to lay out a simple system to set aside the right amount for taxes. So let’s move into our five easy steps.

Step One: Mindset

The first step in particular is extremely important, and that is commitment. We all know that to make change, you need to commit to it because we work with people all the time helping them to commit to the changes they want to make. That applies to all of us too. Ninety-five percent of this system of putting aside taxes that I’m going to show you depends on consistency.

In order to follow through from month to month, it’s not just getting excited and starting, but it’s getting excited and starting and continuing and continuing and continuing and continuing every month or every couple of weeks. Whatever interval you decide is right for you to make sure that this is being taken care of on the regular.

There’s short term pain there. If you’re not used to setting aside money for taxes, if you’re used to spending all the money in your business as though it’s your income, and you’re used to just being able to spend your private practice money on whatever you want whenever you collect a chunk of money, then this is going to hurt at first. I’m going to show you how to earmark some of that money and put it aside. In that short term pain, there is serious long term gain.

There’s also a serious mindset piece here. From every dollar you earn, a portion belongs to the government for the services everyone uses, like roads, schools, libraries, community centres, police, fire fighters, etc. You may not have noticed that so much as an employee because someone managed that for you, but this is an important part of the society we live in. So, think about all of the public services you use and remember that we are all paying for these things. Your money is not really your money.

Step Two: Figure Out Your Tax Rate

To help you figure out your tax rate, here are two websites:

For the United States: www.smartasset.com/taxes/income-taxes

For Canada: www.simpletax.ca/calculator

There are SO many calculators out there, but these are two that I have found and that I like. They are pretty straightforward and let you calculate your taxes quite easily.

One thing that can be confusing about taxes is that when people talk about taxes sometimes they’re talking about the marginal tax rate and other times they’re talking about the average (or effective) tax rate.

If you are starting to feel overwhelmed, take a moment to take some deep breaths. This stuff can be daunting, but I just want to tell you what the difference is between these two things. However, we’re only going to be using one of these as we talk about how to calculate how much money to put aside. So don’t worry, you don’t have to memorize this, but it’s good to know that there is a difference between the two.

The marginal tax rate is a series of tiers and it means that every new dollar above a certain tax bracket will be taxed at that tax rate. In most places in Canada and the United states, the first $12,000 or so is not taxed at all. So if you make $12,000 this year, you won’t have to pay any tax on that. The next level is about $25,000, which will be taxed at a certain rate (a lower rate than higher tiers) – but you will only pay that tax rate on the amount above $12,000. The next tier is for income that falls between $25,000 and $40,000, which has another slightly higher tax rate, but again you will only pay that higher tax rate on the amount above $25,000.

So, if you were to find yourself in the tax bracket that is charged 45% tax – that is NOT the percentage of tax you have to pay on every dollar. Your tax rate is far, far lower than that.

This is why it’s much easier to think of your tax rate in terms of the average (or effective) tax rate. The average (or effective) tax rate is the average tax you pay on every dollar you make. This is the rate that we are going to be using as we make these calculations.

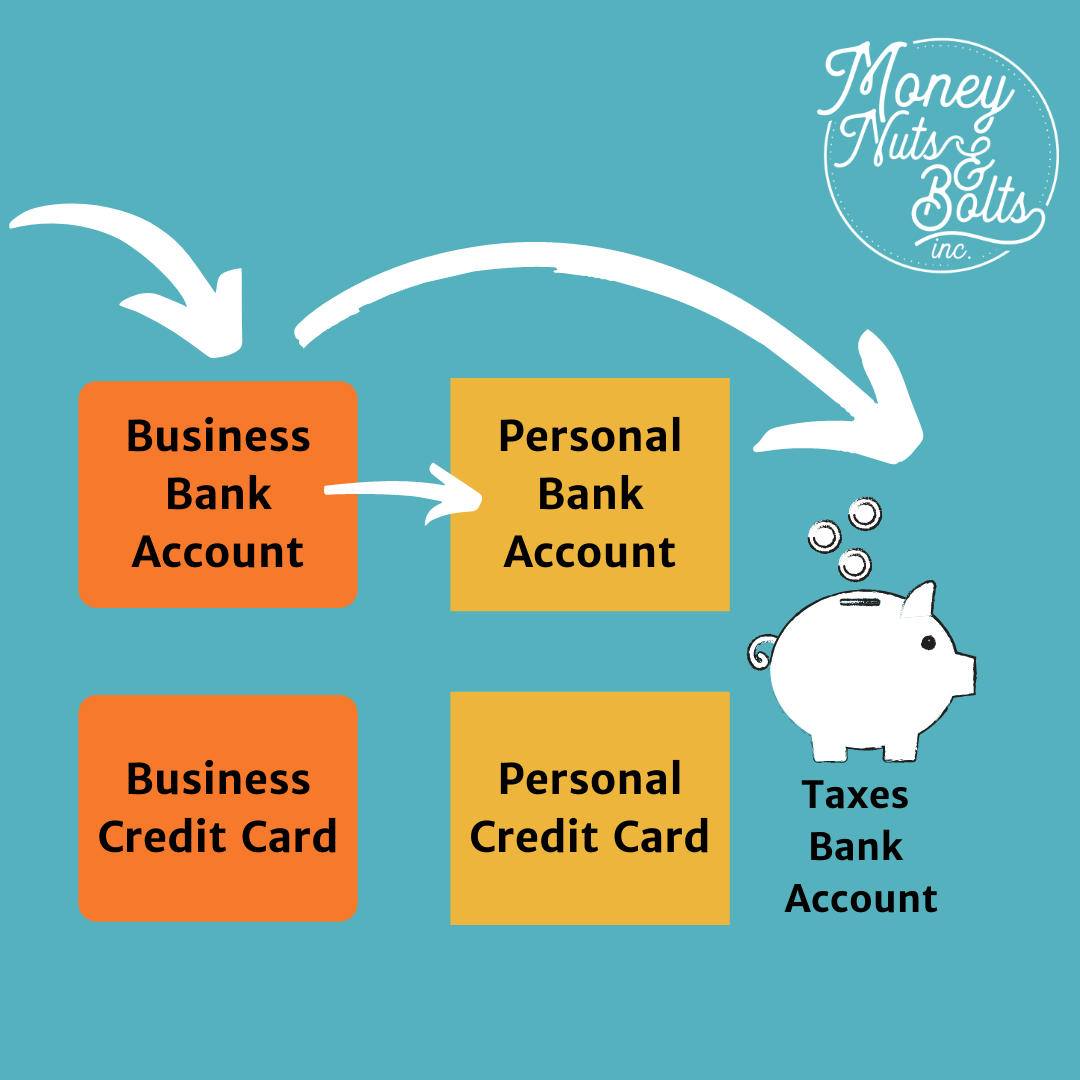

Step Three: Create a Separate Bank Account

This is a super important step for a lot of us. Creating a separate bank account to put your tax money into makes your money so much clearer.

Most of us would look at the balance in our bank account and maybe we know that a certain amount should be saved for something – whether it is taxes or something else – but, psychologically, we will still treat it as if it’s the full amount. So, when an amazing opportunity comes up that requires us to spend a chunk of money, we don’t necessarily protect the money we know we need to save. And before you know it, your tax money has been spent on a training or a trip to a cottage with friends.

Once that money is mingled, it can be very difficult to keep it separate. Intellectually and emotionally, it can be very enmeshed.

Having a separate bank account is such a simple thing to do that it’s so worth making that adjustment. Depending on your bank, it might just be a matter of going online or calling in and making the request. Most banks have made this a super speedy process. It’s totally worth your time to do this.

A separate account gives you a clear place to put your money where you can see it, but where it’s also a little bit further out of reach and less vulnerable to an impulse decision. It means having to transfer the money out of your tax account into your main account to spend it. It also means that when tax time rolls around, you know exactly how much you have saved to remit to taxes annually or quarterly.

Even for myself, being a finance nerd who loves to track every transaction, I have different accounts for different things and it helps to keep things very clear.

The more money we have at our fingertips, the more we spend – that good old lifestyle creep. Putting tax money out of reach means that we have less money to “work with” in our main account and this can actually make us more mindful of our spending as well. This is just human nature.

In terms of the process for a separate bank account, you should send the money to your tax bank account directly from your business bank account. On that note, if you don’t already have a business bank account that is separate from your personal bank account, then you should do that as well. This makes life SO much simpler. It prevents that mingling of your business transactions and personal transactions. So at tax time, even if you don’t track anything at all, all of your business transactions are all in your business bank account and business credit card. You don’t have to go digging through your account to figure out which is personal and which is business, or go finding receipts.

Step Four: Calculate How Much You Need to Set Aside

I have created a tool to help you get clear on exactly how much money you need to be saving for taxes.

[[[[[insert opt-in email for free calculator tool]]]]]]

By putting in your revenue (the total amount of money your private practice has earned before taxes or expenses), your business expenses, and your estimated average tax rate, you will be provided with a total to set aside for taxes for the year. This might look like an overwhelming number, so I’ve designed the calculator to also break it down into monthly and weekly amounts.

Note that there are three different calculators in the spreadsheet document – separated on different tabs along the bottom of the workbook. This is because Single Americans, Married Americans, and Canadians (who always file individually) each have slightly different calculations to make.

For example, in the United States, you also pay Self-Employment Tax, so I have included that in the two American calculators. By comparison, Canadians who are self-employed have to contribute to the Canadian Pension Plan (CPP), so I have accounted for that in the Canadian calculator.

These calculators are a great place to start for figuring out how much to save for taxes. However, I will add the caveat that an accountant might be able to help you find additional deductions that would help you lower the amount you owe.

Step Five: Put the Money Aside

Habits are the best! We know from working with our clients that small changes add up over time into big changes. The same is certainly true for business finances.

Choose a regular interval that works for you to sit down with your finances, make the proper calculations, and put the money into your tax account. It could be weekly, biweekly, monthly, or based on when you do your other admin tasks. It’s important to pick a frequency that doesn’t overwhelm you, but also one that keeps the task manageable instead of letting it build up into a big intimidating snowball.

If you know that you would be tempted to spend any “extra” money in your account, then it might be worth considering doing this more often. That way, you move over the money for taxes into its designated account more frequently so that it doesn’t pile up in your account and look tempting.

Make it a habit and little by little, you’ll set aside all you need.

Then, you send it off! Established businesses have to remit taxes quarterly while new businesses have the option of holding onto it until tax time in their first year. That being said, it can be nice to pay quarterly so that the saved money is out of sight and out of mind.

It’s important to update your numbers if your income changes part way through the year. If you realize that you’re going to end up earning a lot more than you did the previous year, or a lot more than you estimated, then go back to the tax calculator. If you don’t do this, then you will still be caught by surprise at the end of the year when you owe the balance of the taxes on that additional income.

Private Practice Taxes

I know it can feel like you’re “losing” so much money to taxes when you see the number in the calculator. But that’s just not true.

Tax money is not your money. It is a necessary part of our society so that we as a community can support our public services. Even if we are privileged enough to not need or use some of those public services, they are still a vital part of our communities.

When you’re experiencing the short term pain of putting aside that money for taxes, remember the long term gains. By putting aside the money now, you will have far less stress at tax time and be able to approach your tax bill with the calm and confidence of knowing you have that money already.

You can do this! If you follow these steps, you can’t fail. Making it a regular habit makes it easier and easier – eventually it becomes automatic. Your future self will thank you!